How we can improve the teaching of financial literacy in high school? And why is it important?

Our report also makes six recommendations to improve financial literacy education in schools. People need a basic understanding of financial concepts to make good financial decisions. Our newly released research found most students generally do not know a lot about personal finance. This includes being able to apply basic numeracy to real-life financial situations, such as making purchasing decisions that are value-for-money and understanding interest on loans and investments.

Our findings were consistent with previous evidence that 16% of Australian 15-year-olds lack even the basic level of financial literacy they need to participate in society. There is evidence that financial literacy in this age group is declining.

This trend is concerning. The senior years of high school are a time when students take on more personal responsibility and financial independence. The financial habits they form then may last through adulthood. Low financial literacy is persistently linked to poorer financial outcomes.

The Australian Curriculum acknowledges students need financial literacy to operate in our financial world. However, this curriculum only covers up to year 10. In years 11 and 12, the years that are particularly important in shaping students’ financial capability, financial literacy is taught only in lower-level maths subjects.

ACER/PISA 2018, CC BY-NC-ND

What did the study find?

Our research explored the financial literacy of students in years 10, 11 and 12 at two urban and two rural schools. We found what students do know about financial literacy has been learned from home, maths or business studies. Students who were undertaking business studies were far more informed than other students.

Home life has been found to have a huge impact on a child’s financial literacy. There are often calls for parents to teach their children about personal finance. However, that assumes parents are able and willing to do that.

The students we spoke to were incredibly diverse. Household structures varied greatly, with many students not living with their parent/s. There was also evidence of parents not being able to provide financial guidance.

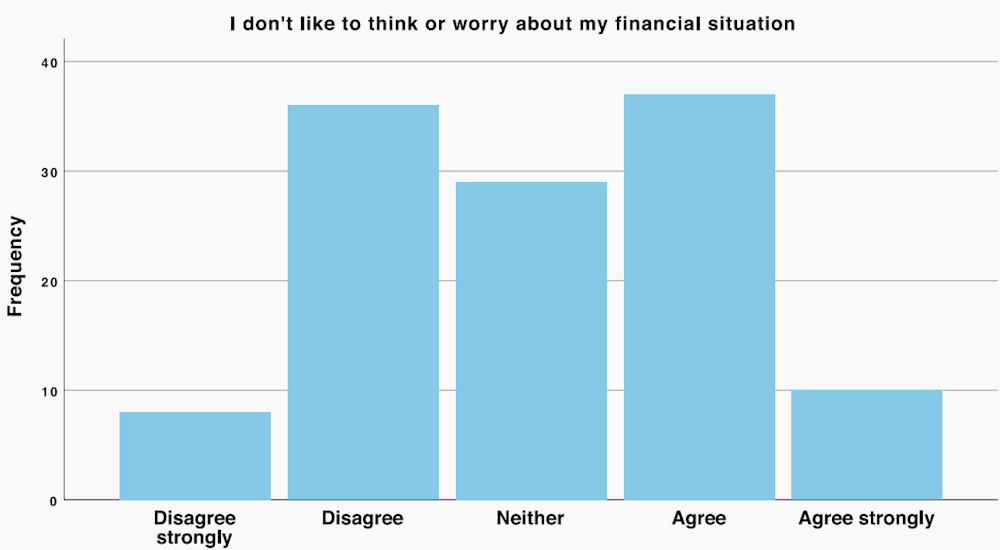

Nearly half the surveyed students preferred not to think about their financial situation.

We talked to a lot of the students about maths and found this was not the most effective curriculum area for learning about personal finance. When taught as part of the maths curriculum it tends to result in students fixating on formulas and calculations, without understanding the underlying concepts. As one student said:

“I only really remember the formula because that’s all we got taught.”

Many students also dislike maths. This means they are disengaged from learning at the outset. One student told us:

“If I was in class doing that [a simple question about interest], I would just read it, keep reading it, but not actually process it or try it because I’d just give up.”

There was also often a disconnect between the financial scenarios students were learning about and their experiences in their own lives.

Students who could remember financial concepts would often recall an experience or something from history when talking about it. This suggests stories may be more effective in communicating financial concepts. For example, one student said of inflation:

“Over time, because obviously more money is being printed […] people think printing money creates more money and you’re richer, when in reality you’re just making the currency you have worthless, because there’s so much of it, that it’s not difficult to acquire it at all. I learned most of that from history.”

Interestingly, we found evidence of young women in particular needing more context to make financial decisions. When asked financial questions, they wondered about different aspects of the question rather than quickly answering. Test questions commonly used to assess financial knowledge often offer little context.

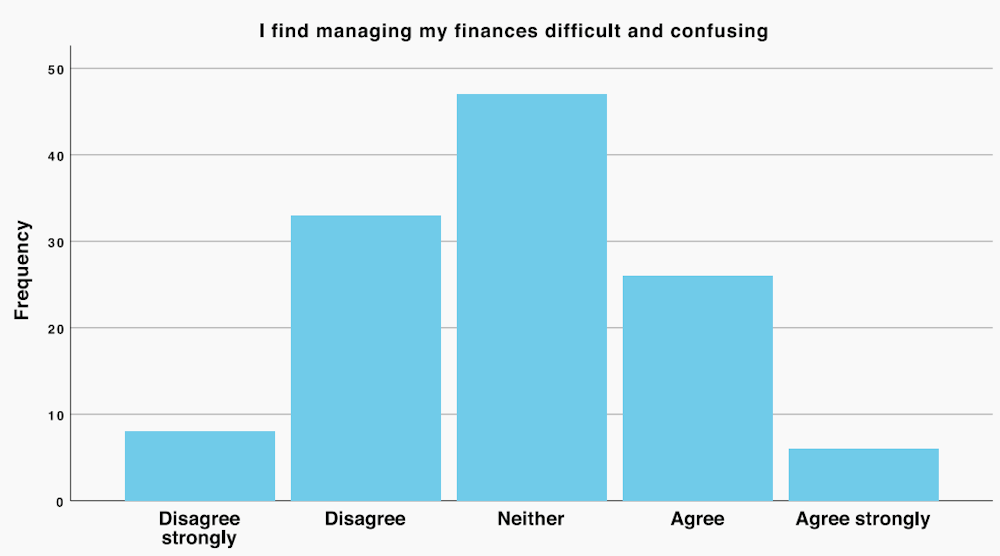

About one in three students agreed they found managing their personal finances difficult and confusing.

Finally, we noted many students were not learning financial strategies, such as moderating spending, that have lifelong benefits.

How can we improve?

Given the importance of financial literacy for student well-being, our report makes these recommendations:

- financial literacy education should be elevated in high schools, ideally as a standalone programme, but also by injecting principles of financial literacy into as many curriculum areas as possible – particularly in the well-being and pastoral care area

- financial literacy education in maths needs to be improved, using a range of approaches – not limited to calculation activities

- financial literacy education should be expanded to subjects other than maths and business, in line with shifting the focus from financial calculations to financial concepts

- learning activities should be aligned with the students’ general level of financial experience

- students need more exposure to effective financial strategies, in particular how to moderate (or control) spending for saving

- a range of assessment methods should be offered to enable students to show what they have learnt. Assessment tasks should go beyond calculations and could include written pieces, visual or dramatic presentations, or oral explanations. These could be presented by groups or individuals.

Laura de Zwaan, Lecturer, Department of Accounting, Finance and Economics, Griffith University and Tracey West, Lecturer in Behavioural Finance, Griffith University

This article is republished from The Conversation under a Creative Commons license. Read the original article.